{kind=link}

POS defies Covid-19 pandemic to remain a game-changer in driving financial inclusion

By Samuel Diala

A recent study by NextMoney Magazine revealed multi-dimensional impacts of the Covid-19 pandemic on Point of Sale (POS) transactions during the three quarters of 2020. And this is important to Nigeria’s fiscal and monetary policy authorities in driving financial inclusion.

The POS is a critical element in Nigeria’s financial services reform that began about a decade ago. It has also proved a key success factor in driving the Financial Inclusion Strategy (NIFS). The NIFS was launched in October 2012 to reduce the large population of the unbanked. The critical role of POS centres on two key benefits namely, creating jobs and driving financial inclusion.

The setback

However, NIFS suffered a setback six years after it was launched. This was due to a myriad of factors ranging from inadequate awareness to structural challenge. The CBN in 2018 admitted that the scheme had lost steam and needed to be reinvigorated. It expressed concerns that the 2020 target year could turn out a mirage, hence the need to revisit and rejig the scheme.

“Overall, Nigeria has failed to meet its financial inclusion targets due to a variety of factors; a step-change in the pace of progress is needed to close the sizeable gap between the current status and the targets. While some notable milestones have been achieved, overall financial exclusion rate stands at 41.6 per cent based on the biennial Access to Financial Services in Nigeria Survey”, the CBN said in a circular signed by its director, Development Finance Department, Mudashiru Olaitan.

According to the apex bank, “Performance did not meet expectations across all inclusion targets for products, channels and enablers. Among product categories, credit, insurance and pension fell short of targets by the most significant margins. Point of Sale (POS) terminals and Automated Teller Machines (ATM) showed the least progress among channels.”

In its exposure draft titled ‘National Financial Inclusion Strategy Refresh’, the CBN said it would collaborate with the deposit money banks and other stakeholders in accelerating the implementation of the NFIS. It was in the programme’s comatose stage that the CBN Governor, Godwin Emefiele’s second tenure began in June 2019. Emefiele promised to accelerate the NFIS towards achieving 95 per cent inclusion by 2024.

“Over the next five years, through initiatives and policy measures such as the Shared Agent Network (SANEF) and the payment service banks, we intend to broaden access to financial services to individuals in underserved parts of the country. Our ultimate objective is to ensure that 95 percent of eligible Nigerians have access to financial services by 2024”, Emefiele assured.

Six months into his second term, the Covid-19 pandemic struck, creating a crisis that resulted in the total lockdown of the economy. However, remarkable progress had been made at the time Covid-19 pandemic occurred in January 2020. There were concerns that the crisis might create a hitch in financial inclusion tempo, especially among the POS operators across the country.

The POS operators belong to the Mobile Money/Agent Banking group that constitute a chunk of micro, small and medium enterprises (MSME) – the engine of the economy. As a result of the uncertainty that surrounded their business at the time, there were concerns that theCovid-19 impact might boost or mar efforts in actualizing the 95 per cent financial inclusion target by 2024.

Experts who expressed this concern focused on the twin grave impacts of the situation: global crisis of a health pandemic and economic shrink from prolonged lockdown. Besides harming the livelihoods of the low-income population globally, they pointed to a long, dark tunnel of devastating economic uncertainty. Covid-19 “is an unparalleled global macro-economic shock of uncertain magnitude and duration. The uncertainty is what makes it so very dangerous,” said Financial Inclusion Advocacy Centre (FIAC) of UK in a report last June.

Imperative, findings

It is, therefore, imperative to ascertain the impact of the global pandemic on POS transactions. This is against the backdrop that the crisis disrupted business activities and created huge economic setback. Focus is on the first three quarters of 2020: January-March (Q1) before lockdown; April-June (Q2) during lockdown; and July-September (Q3) after lockdown – when gradual relaxation of restrictions was effected. This is against the backdrop of rising confirmed case of the pandemic which hit global peak of 45.24 million and death toll of 1.18 million as of October 31, 2020. Nigeria recorded 62,964 with 1,146 deaths during the period,representing 1.8 per cent of confirmed cases across the country.

Data from the Nigeria Inter-Bank Settlement System (NIBSS) shows that POS plays a key role in driving the financial inclusion strategy. The alternative payment channel has maintained an exponential growth in the past four years – in value, volume, registration and deployment. NextMoney findings revealed that Covid-19 crisis had mixed impacts on POS facilities – minimal in the aspects of transaction in volume and value only. But there was overall accelerated tempo.

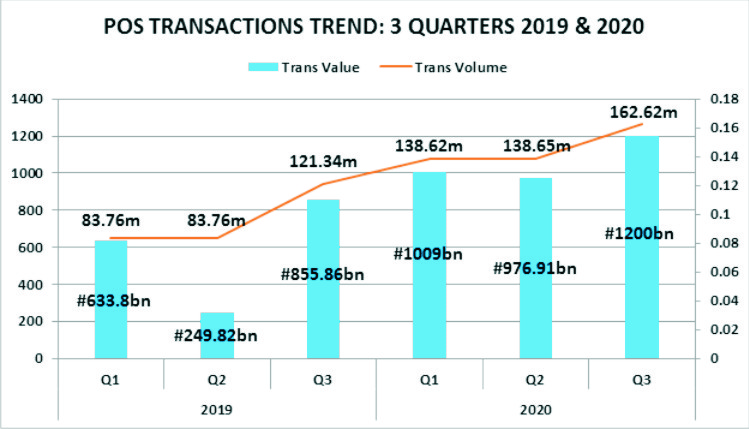

Analysis of the findings showed that POS transactions Value which recorded N1.009 trillion in the first quarter of 2020, dropped by N32 billion to N976.91 billion in the second quarter during lockdown, representing 3.17 per cent; to climb by N223 billion to N1.20 trillion in the third quarter or 22.82 per cent. The N3.18 trillion total transaction Value for three quarters of 2020 was 83 per cent compered to N1.74 trillion in the corresponding period of 2019.

Transaction Volume of 138.62 million in the first quarter did not record significant change in second quarter of 2020 hit by the Covid-19 lockdown. The figure for second quarter was 138.65 million showing severe impact of the lockdown on businesses. Most businesses that use POS for transactions were forced to shut down their operations and close their physical offices following the restriction of movement ordered by the government.

However, activities picked up in the third quarter with transactions Volume hitting 162.62 million – a difference of 23.97 million representing 17.38 per cent rise. Total Volume for the three quarters was 400 million as against 289 million for the corresponding period of 2019 representing 38 per cent upward trend. The rise was occasioned by the return of most businesses and companies to the normal working hours attended before the coronavirus outbreak. Findings also showed that many people resorted to POS business as alternative activity to sustain their means of livelihood hit by the lockdown.

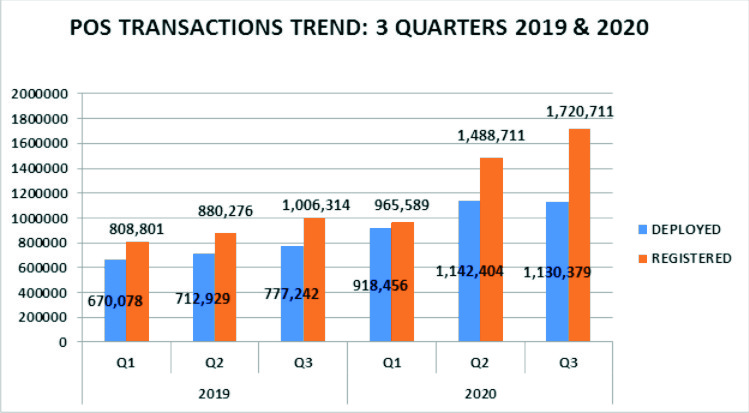

This can be deduced from the number of POS terminals registered and deployed during the periods under review. While transactions Value and Volume showed no increase in the second quarter of 2020 which was the peak of the lock down, the numbers of POS registered and deployed rose from 965,589 and 918,456 to 1,488,711 million and 1,130,379 million, representing 54.17 and 23.2 per cent respectively.

When compared with the corresponding period of the preceding year, POS registered and deployed showed 55.0 per cent and 47.77 rise per cent: from 2.7 million to 4.17 million and 2.16 million to 3.12 million, respectively.

To substantiate the findings, NextMoney conducted a two-week physical field survey of POS operators in the six sub-divisions of Alimosho Local Government Area of Lagos. Alimosho, the largest LGA in Lagos, has six Local Council Development Areas (LCDAs): Agbado/Oke-odo, Ayobo/Ipaja, Alimosho, Egbe/Idimu, Ikotun/Igando and Mosan Okunola. The survey was done through random sampling of the areas using the Google Map as a guide in choosing the areas to sample. The aim was to determine the rate of increase in new POS operators after the lockdown, and the reason for going into the new business.

Out of 200 operators interviewed, 28 were new entrants, representing 14 per cent. Nine of them said they joined the business to augment their income following impact of the Covid-19 lockdown, three said they are employees while two would not disclose their status. Most POS customers interviewed attributed their patronage to convenience, proximity, reliability and availability. “It saves me the trouble of queuing at the banks’ ATM for hours; many a time, the ATM facilities are not functional. This can be frustrating,” said Manny Ekemela, a car dealer at Igando.

The aftermath of the pandemic crisis tremendously added a fillip to the alternative payment channel and became a boost to financial inclusion. The renewed vigour indicates a rapid drive of the financial inclusion project, according to reports by the NIBSS, during and after the peak of the Covid-19-induced lockdown.

It is a good sign that POS transactions did not suffer any setback of considerable dimension arising from the crisis. This suggests that a greater number of people are embracing the POS as alternative payment system. It is also an indication that the poor service delivery of the banks’ ATM terminals most of the time, forceed financial services consumers to patronize the POS operators.

Again, the drive for urban-rural migration added to the city pressure. This is compounded by pollution, high cost of living, dwindling income-generating opportunities, multiple taxation, traffic jam and other social pressure. All these contribute to forcing people to look homewards. The increased in local businesses creates opportunity for POS transactions which dot shops and other premises in the rural areas. This is on the heels of banks de-emphasizing rural bank branches which used to be the trend some decades ago.

The NBISS in its 2020 half year report stated that POS transactions which hit N1.64 trillion in the first five months of 2020 was the highest in four years. The value of transactions done across POS channels in Nigeria increased from N1.14 trillion recorded between January and May 2019 to N1.64 trillion within the same period in 2020.

The report implies that the total value of transactions from POS machines rose by N500 billion, which represents a 43.8 per cent increase in five months. The total volume of POS transactions also increased from 152.6 million to 228.86 million within the period under review. This indicates that the volume increased by 76.26 million, or 49.9 per cent.

A Labour Economist, Benneth Ujah, told NextMoney that rising rate of unemployment is forcing many Nigerians within the labour force to look for alternative means of livelihood aside paid employment. “This shutdown caused the steady growth in demand for alternative payment, which POS business has benefited from. Mobile Money and Agent Banking operators, as small businesses, will respond to the situation naturally”, he said.

According to data published by NBS in its “Labour Force Statistics: Unemployment and Underemployment Report for Q2 2020”, Nigeria’s unemployment and underemployment rates worsened significantly since the third quarter of 2018 (Q3 2018) when the last report was issued – from 23.1 per cent to 27.2 per cent; and 20.1 per cent to 28.6 per cent respectively.

During the period, total number of unemployed Nigerians increased from 20.92 million to 21.96 million from a labour force of 90.47 million to 80.29 million (labour force constitutes people within ages 15-64, who are able and willing to work). Working age of 25-34 years recorded the highest number of unemployed persons followed by those in age bracket 15-24 years: 7.16 million and 6.81 million, respectively.

Evidently, the Covid-19 pandemic impact has created rapid expansion in POS transactions. The contribution of POS channel to the Mobile Money and Agent Banking sub-sector is significant in facilitating the financial inclusion initiative.

- This investigation was supported by the US Embassy via the ATUPA Fellowship by Civic Hive